Why Reconciling Accounts Monthly Is the Secret to Accurate Financial Reporting and Better Cash Flow

By Louisa

4 Views

Maintaining accurate financial records is essential for every business, regardless of its size or industry. One of the most effective ways to keep your books organized and your finances under control is by reconciling accounts monthly. Although it may seem like a routine bookkeeping task, monthly reconciliation has a direct impact on cash flow, financial reporting, budgeting, and long-term business success.

When accounts are not reconciled regularly, small mistakes can go unnoticed for months. These inaccuracies may lead to incorrect financial reports, poor business decisions, tax preparation issues, and unnecessary financial stress. By making reconciliation part of your monthly accounting process, you gain confidence that your financial records accurately reflect your business activity.

This guide explains why monthly account reconciliation matters, how the process works, and the benefits it offers to business owners looking to improve financial management.

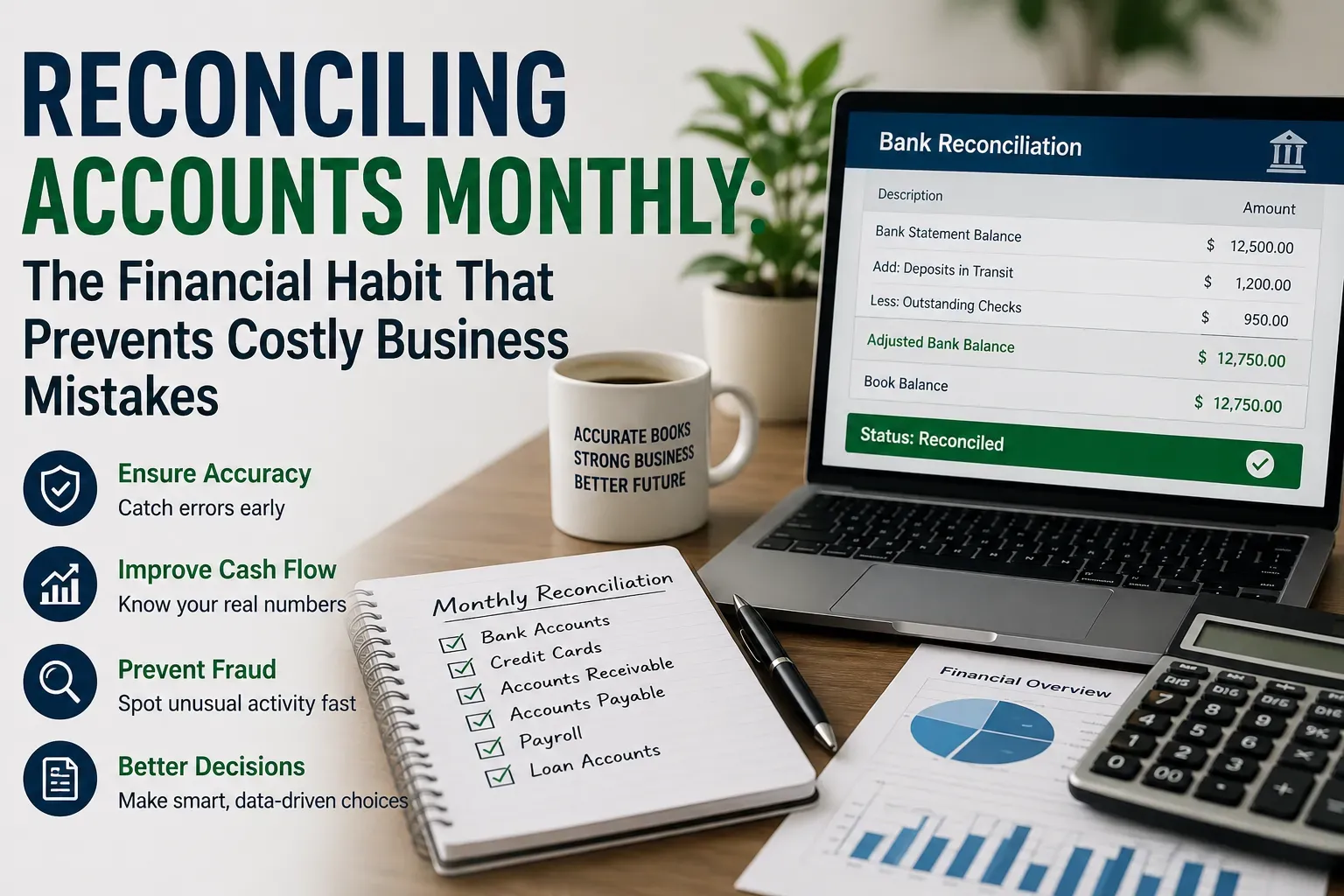

What Is Monthly Account Reconciliation?

Monthly account reconciliation is the process of comparing your accounting records with external financial documents to verify that every transaction has been recorded correctly.

This typically includes matching:

- Bank statements

- Credit card statements

- Payment processor reports

- Loan balances

- Payroll records

- Accounts receivable

- Accounts payable

The purpose is to identify missing transactions, recording errors, duplicate entries, bank fees, and timing differences before they become larger financial problems.

Why Businesses Should Reconcile Accounts Every Month

Financial data changes every day. Waiting until the end of the year to review your books makes it much harder to correct mistakes and understand your financial position.

Monthly reconciliation helps businesses stay informed while maintaining accurate accounting records throughout the year.

Some of the biggest advantages include:

More Accurate Financial Records

Reliable bookkeeping begins with accurate data.

Reconciling your accounts every month ensures that your accounting software reflects actual bank balances and business transactions. This creates trustworthy financial statements that can be used for planning, budgeting, and decision-making.

Better Cash Flow Management

Cash flow is one of the most important indicators of business health.

Monthly reconciliation helps you monitor:

- Incoming customer payments

- Vendor payments

- Outstanding invoices

- Bank fees

- Automatic withdrawals

- Available cash

Knowing where your money is going allows you to make smarter financial decisions and avoid unnecessary cash shortages.

Faster Error Detection

Mistakes happen in every business.

Transactions may be entered twice, categorized incorrectly, or omitted completely. Banks may occasionally process charges incorrectly, and payment processors may report unexpected adjustments.

Monthly reconciliation helps detect these issues while they are still easy to investigate and correct.

Improved Tax Preparation

Keeping your books updated throughout the year makes tax season significantly easier.

Instead of spending weeks reviewing old transactions, you'll already have organized financial records that support accurate income reporting, deductible expenses, and tax compliance.

This can reduce preparation time and minimize the risk of filing errors.

Common Accounting Issues Monthly Reconciliation Prevents

Regular reconciliation helps eliminate many financial problems before they affect your business.

Examples include:

- Duplicate expense entries

- Missing deposits

- Incorrect account balances

- Outstanding checks

- Payroll mistakes

- Vendor billing discrepancies

- Unrecorded bank charges

- Data entry errors

- Missing customer payments

- Incorrect financial reports

Identifying these issues every month keeps your books accurate and reduces costly corrections later.

A Simple Monthly Reconciliation Checklist

Following a consistent process helps improve efficiency and accuracy.

Review Bank Statements

Compare every deposit, withdrawal, transfer, and service fee against your accounting records.

Investigate any transactions that cannot be matched.

Verify Credit Card Transactions

Review employee expenses, recurring software subscriptions, office purchases, and travel expenses.

Confirm each charge has supporting documentation and has been categorized correctly.

Check Customer Payments

Match customer payments with outstanding invoices.

Follow up on overdue balances to improve collections and maintain healthy cash flow.

Review Vendor Payments

Confirm supplier invoices have been recorded correctly and that payments match the amounts shown on statements.

Compare Ending Balances

After reviewing all transactions and making necessary adjustments, your accounting records should agree with your financial institution's ending balance, allowing for legitimate timing differences.

How Monthly Reconciliation Supports Better Business Decisions

Business decisions should always be based on reliable financial information.

When accounts are reconciled consistently, business owners can:

- Monitor profitability

- Track operating expenses

- Measure business growth

- Identify spending trends

- Forecast future cash flow

- Create realistic budgets

- Evaluate investment opportunities

- Improve financial planning

Without accurate bookkeeping, even well-intentioned decisions can be based on misleading numbers.

The Role of Technology in Account Reconciliation

Modern accounting software has made reconciliation more efficient than ever.

Many bookkeeping systems now offer features such as:

- Automatic bank transaction imports

- Intelligent transaction matching

- Duplicate transaction alerts

- Reconciliation reports

- Digital document storage

- Secure cloud access

While automation reduces manual work, every reconciliation should still be reviewed by someone who understands your business finances. Human oversight remains essential for identifying unusual transactions and maintaining accounting accuracy.

Mistakes to Avoid During Monthly Reconciliation

Businesses often create unnecessary problems by overlooking small details.

Avoid these common mistakes:

- Delaying reconciliation until year-end

- Ignoring small bank fees

- Forgetting electronic payments

- Not reviewing payment processor activity

- Posting expenses to incorrect accounts

- Making adjustments without documentation

- Failing to reconcile credit card accounts

- Overlooking uncleared transactions

Creating a monthly routine significantly reduces the likelihood of these issues.

Should You Handle Reconciliation Yourself?

Many entrepreneurs begin by managing their own bookkeeping. As transaction volume grows, reconciliation becomes more complex and time-consuming.

Working with experienced bookkeeping or accounting professionals can provide several benefits:

- Greater financial accuracy

- Faster month-end closing

- Better financial reporting

- Improved tax readiness

- Reduced administrative workload

- More time to focus on business growth

Professional support also helps ensure accounting standards are followed consistently throughout the year.

Best Practices for Successful Monthly Reconciliation

To get the most value from reconciliation, follow these practical habits:

- Complete reconciliations every month without skipping periods.

- Keep digital copies of receipts and financial documents.

- Record transactions promptly instead of waiting until month-end.

- Review financial statements after each reconciliation.

- Resolve discrepancies immediately.

- Use reliable accounting software for transaction tracking.

- Maintain consistent bookkeeping procedures.

These practices improve financial accuracy and create a stronger foundation for long-term business success.

Final Thoughts

Reconciling accounts monthly is far more than an accounting task—it is a proactive financial management strategy that helps businesses maintain accurate records, strengthen cash flow, reduce errors, and make informed decisions with confidence. By reviewing your accounts regularly, you can identify discrepancies early, improve financial reporting, simplify tax preparation, and gain a clearer understanding of your company's overall financial health.

Whether you manage bookkeeping internally or work with an accounting professional, making monthly reconciliation a consistent habit can save time, reduce costly mistakes, and support sustainable business growth for years to come.

Related Reading

Top 10 Hidden Secrets About Business & Finance You Need to Know

Welcome to our in-depth exploration of Business & Finance. In an era defined...

Why Business & Finance is Transforming the Global Industry Landscape

Welcome to our in-depth exploration of Business & Finance. In an era defined...